Summary of AB InBev's 2nd Quarter of 2023 with My Analysis

Strong Results Despite Weakness in U.S. Following Bud Light Boycott | Lowering PT to $81

Summary

AB InBev reported earnings for the 2nd quarter on August 3rd. Non-GAAP EPS was 72 cents, beating estimates by 3 cents. Revenue was $15.1 billion, missing estimates by $260 million.

The company's net leverage went up to 3.7x from 3.51 at the end of 2022. Margins are still under pressure due to elevated raw material costs but management expects this to ease in the 2nd half of the year.

Due to lower sales and cash flow generation from the U.S. region, I am lowering my price target to $81. This is derived from a revised 4.2% growth rate, down from 5% previous, and a revised multiple of 18, down from 20, in my model. Based on free cash flow, it is an 18x multiple on a 5-year average of free cash flow, excluding 2020 due to the abnormal circumstances of the year.

Exhibit A: Valuation

Source: Company Filings, My Calculations

Regions were strong outside the U.S. with South Korea coming in weaker than expected. Volumes were down but pricing was up, which helped drive revenues higher year-over-year. All other regions outside the U.S. and South Korea were strong.

Strong Regions

Mexico and Columbia had a strong performance during the quarter. Mexico had double digit top and bottom-line growth, and Columbia had high single digit revenue growth and double-digit bottom-line growth.

Brazil had high single digit revenue growth and double-digit bottom-line growth. In the South America region, net revenue increased 24% and EBITDA increased 47.2%. Total volumes were down 1.9%.

Europe was a positive with high single digit top line growth and bottom-line growth. South Africa was a positive as well with double digit revenue growth. Overall, the EMEA region had 12% revenue growth and 7.2% EBITDA growth.

China was another positive with double digit revenue and bottom-line growth. The Asia Pacific region had net revenue growth of 14.5% and EBITDA growth of 10.7%.

Exhibit B: Organic Revenue and EBITDA Performance By Region

Source: Company Filings

North America Was Weak Due To U.S.

Results from the U.S. came in weak following the boycotts but it wasn’t as bad as I expected. Revenue declined by 10.5%, sales-to-wholesalers declined by 8.6% and sales-to-retailers declined by 9.2%. Canada performed better with low-single digit revenue growth, but volumes declined mid-single digits.

Overall, the North America region saw total volumes decline 14.1%, net revenue decline 9%, and EBITDA decline 24.4%. Management said that market share has been stable since April and they will take initiatives, such as increasing their summer marketing budget, to regain market share. I don’t believe the company will fully recover all the market share they lost.

Exhibit C: U.S. Market Share Since April 2023

Source: Company Filings

Deleveraging Slowed

Debt deleveraging slowed following the slowdown in the US market and due to working capital. The decline to changes in working capital was due to the company paying down its accounts payable balance. The company paid down $1.1 billion more in payables for the first six months of 2023 than it did in 2022. The CFO explained on the call that payables match inventories, and this will adjust in the second half.

The accounts payable balance has increased materially over the last four and half years. Part (or most?) of this should be due to inflation, but a $7B increase going back to 2019 is a meaningful increase in 3.5 years, especially since the company hasn’t been acquiring companies during this timeframe, but has actually been shrinking its beer empire. It raises the following questions to keep in mind since deleveraging and free cash flow generation are a big part of my thesis:

1. Is the increasing DPO a positive sign of ABI’s moat or a concern to free cash flow generation?

2. Will the increasing DPO strain supplier relationships?

3. Will DPO continue to increase or it will go back down like it did in 2021 and 2022?

4. Will raw material costs decline in the second half, as management is expecting, and will they decline beyond 2023 as well?

Exhibit D: Accounts Payable And DPO Is Increasing

Source: Company Filings, My Calculations

On a bright spot, management confirmed that they feel confident that they can sustain their 4% interest rate on the debt despite the higher interest rate environment, although, I don’t think this was a surprise since 96% of the debt is fixed at 4% and the company has at least two more years to go in its deleverage phase. At the end of the quarter, net debt/EBITDA stood at 3.7x compared to 3.5x at the end of Q4 22, a slight increase.

Exhibit E: Change In Working Capital Increased Year-Over-Year

Source: Company Filings

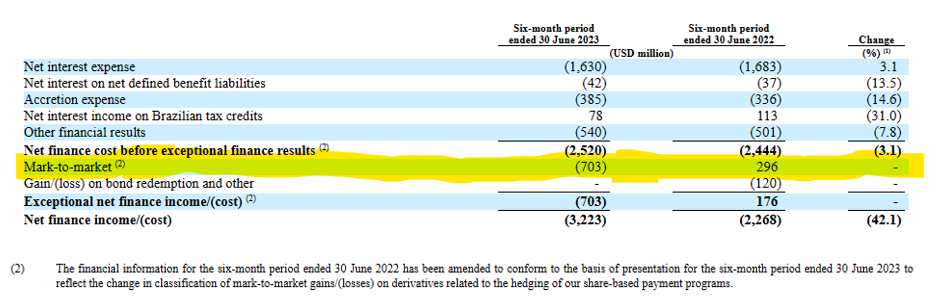

Net Finance Costs Effect On GAAP Income

Ab InBev had a $1.2 billion drop in GAAP net income year-over-year. The majority of this decline was due to a negative mark-to-market adjustment on the share hedges that the company entered to hedge the share payments the company issued during the acquisitions of Modelo in 2013 and SAB in 2016.

These mark-to-market adjustments aren’t reflected in the company's adjusted earnings since they aren’t related to the company’s business operations. Although it's only a loss on paper, since they're marked to market, these hedges still reflect an allocation of capital.

The mark-to-market adjustment was negative $703 million during the year compared to a gain of $296 million in Q2 2022. SG&A during the quarter was $200 million higher year-over-year due to higher SG&A expense, likely resulting from the increasing marketing in the U.S.

Exhibit F: Net Finance Cost Reconciliation

Source: Company Filings

Conclusion

The boycott that ensued after a March Madness marketing campaign will go down as one of the worst marketing outcomes to date. My BUD thesis was based on strong brand values, which come from economies of scale that allows the company to invest a lot more in marketing than its competitors.

Since the company suffered such a large loss in earnings and brand value in the US, I lowered my price target on lower free cash flow and earnings growth, and a lower multiple due to a reflection that the company's moat in the US isn’t as strong as I initially thought it was. The moat in all other regions is still strong though, but the US demonstrates a higher probability that this could change in the future.

Despite these concerns, the drop in the stock price over the last couple months still offers a good prospective return at around $56-$58.