Has Wealth-to-GDP Begun to Mean Revert?

Summary of Absolute Return Partners' February 2023 Letter

Intro

This letter will discuss whether or not all of Niels’ talk in his past letters about the Wealth-to-GDP ratio was overstated or if it really is significant.

Niels’ talk about the Wealth-to-GDP ratio has focused on the following points:

1. Wealth cannot continue to grow faster than GDP.

2. The Wealth-to-GDP ratio must revert to its long-term average sooner or later.

These points apply to the Wealth-to-GDP ratio all over the world, but Neils focuses only on the U.S. because that is where the ratio has been significantly higher compared to other countries and the U.S. has provided trustworthy data going back to 1951.

Exhibit A: U.S. Wealth-to-GDP*

*As of September 2022. Data on wealth for December 2022 won’t be published until March 2023.

Source: Absolute Return Partners

Although the Wealth-to-GDP ratio in the U.S. had a large drop in Q4 22, it then saw a reversal in the first few weeks of 2023 as equity markets quickly rose higher. This isn’t captured in Exhibit A since updated data on wealth isn’t available yet.

The Argument For Wealth-to-GDP To Continue Falling

The latest reading of Wealth-to-GDP as of September 2022 is 5.57 times. This is still well above the average of 3.8 times, as you can see from Exhibit A.

Therefore, there is still a lot of downside (30%) despite the ratio already falling 10% from the previous high that was set in 2021.

This downside is likely to come from the value of private businesses, whose values lag public equity markets, and from property markets whose values are more vulnerable to rising interest rates. Keep in mind that property prices are the biggest driver of household wealth in most countries.

The recent equity rally should be taken with a grain of salt since the U.K. is probably already in a recession; Continental Europe is on the edge of a recession; and macroeconomic data are signaling that the U.S. will enter a recession in the 2nd half of 2023.

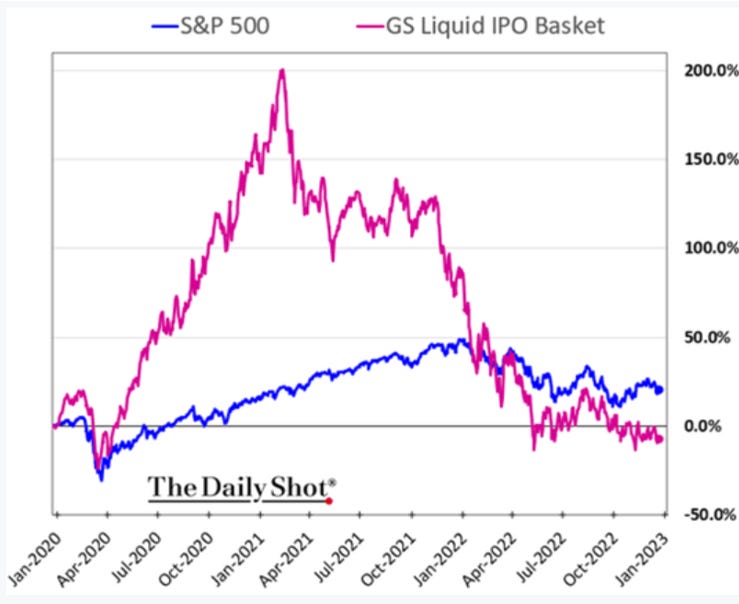

Even though earnings estimates and equity valuations in the U.S. aren’t reflecting a recession yet, Niels says that the performance of the Initial Public Offering (IPO) market in the U.S., which Niels says is a good indicator of investor sentiment, has been pessimistic in 2022.

The underperformance of IPOs was even adjusted by Niels for the heavy weight that the IPO market has toward technology.

Exhibit B: Performance of S&P 500 and GS Liquid IPO Basket

Source: The Daily Shot; Absolute Return Partners

The Counter Argument for Wealth-to-GDP To Continue Falling

There is a counterargument for the U.S. entering a recession and the GDP-to-wealth ratio declining though.

The consensus forecast for U.S. GDP growth for this year is up again.

Exhibit C: Consensus Forecasts for 2023 U.S. GDP Growth

Source: The Daily Shot; Absolute Return Partners

The catalyst to focus on here is inflation though. If inflation continues to come down then the Fed will most likely stop hiking rates. If rates hikes stop then this could be a catalyst for the market to continue rallying. Does Niels believe that inflation will continue to come down and the Fed will stop hiking rates though?

Summary

The answer to that last question is no. Niels expects the Fed to struggle to bring inflation down below 5%. This is going to lead to the Fed increasing rates again and eventually resulting in equity market declines later in the year.

He expects the Fed to struggle bringing inflation down below 5% because most of the inflation in the U.S. today is in core inflation. Core inflation doesn’t include energy and food where prices are more volatile.

But Niels warns that two consecutive years of negative returns in U.S. equity markets almost never happen so keep in mind that if this plays out as he expects then the second round of Fed hikes will lead to more equity declines this year, but it could be a good buying opportunity since markets could recover at the end of the year.